Why Electronics Prices Are Rising: RAM, Processors, & the Global Supply Chain Crisis (With Energy & Nuclear Power Linkages)

These increases stem from systemic global supply chain shifts, geopolitical pressures, rising energy costs, and long-term demand growth for semiconductors across consumer, enterprise, and AI infrastructure markets.

7 min readEr.Muruganantham

Electronics prices — especially RAM, processors, GPUs, and system-level silicon — have seen sustained increases over the past few years. These increases are not random or short-lived fluctuations; they stem from systemic global supply chain shifts, geopolitical pressures, rising energy costs, and long-term demand growth for semiconductors across consumer, enterprise, and AI infrastructure markets.

This blog explores:

- What is happening

- Why prices are rising

- The root causes

- Current economic and tech symptoms

- Energy implications including nuclear power debates

- Nvidia founder Jensen Huang’s statements

- India’s move to open nuclear power to the private sector

- What this means for consumers and industry

1. Root Causes of Rising Electronics Prices

Electronics price inflation is driven by a mix of supply and demand pressures:

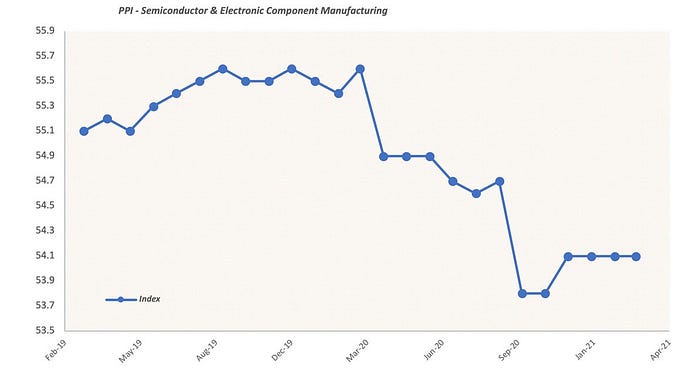

a. Global Semiconductor Supply Chain Complexity Semicon manufacturing depends on a highly specialized and interdependent supply ecosystem that spans geology (rare earths), fabrication (fabs), design (EUV tools), packaging, and global logistics. Disruptions in any link — from Taiwan’s semiconductor hubs to Japan’s materials — reverberate across the entire chain, increasing scarcity and pricing. ORF Online

b. Strong Demand for Advanced Chips Demand for AI accelerators, edge computing chips, and high-performance processors has surged. Data centers, automotive, IoT, and mobile ecosystems compete for the same limited fabrication capacity, especially at leading foundries like TSMC, Samsung, and Intel.

c. Slow Capacity Expansion Building new semiconductor fabs — especially for leading-edge 5nm, 3nm, and beyond — requires years and billions of dollars. Meanwhile, demand curves have steepened fast due to AI, EVs, and cloud services, creating a structural mismatch.

d. Geopolitical Restrictions Export controls on advanced lithography and chips restrict supply to certain countries. While designed for strategic advantage, these controls reduce the global pool of available high-end silicon, putting upward pressure on prices.

e. Energy Costs and Infrastructure Constraints Chip manufacturing, data centers, and system integration are energy-intensive. Power costs are a non-trivial part of operating expenses. As energy prices rise or become unstable, some manufacturing costs get passed down the value chain.

2. What Consumers Notice Right Now

You may already be seeing clear symptoms of this pricing pressure:

- Retail prices for RAM modules remain elevated despite typical seasonal declines. Inventory is lean as manufacturers allocate stock to enterprise and OEM channels first.

- Processor and GPU prices stay high post-launch, especially AI-oriented silicon like Nvidia GPUs used in data-centric workloads.

- Lead times on components still stretch weeks to months, especially at mid- to high-end specifications.

- Used electronics markets heat up as new device prices rise.

These symptoms are not localized to one region — they are visible in North America, Europe, and India simultaneously.

3. Impact on Industries and Consumers

a. Consumer Electronics Higher prices for RAM and CPUs directly affect laptop, smartphone, and gaming PC pricing, reducing affordability especially for price-sensitive markets.

b. Enterprise IT & Data Centers Corporations face higher CapEx for servers and storage. Elevated silicon costs can delay refresh cycles, slow AI deployment strategies, or push organizations to adopt second-hand or cloud resources where possible.

c. Automotive & IoT Cars increasingly rely on advanced chips for ADAS, infotainment, and connectivity. Elevated electronics prices affect vehicle production costs and pricing strategies.

d. Startup and R&D Budgets Startups and research institutions face higher barriers to entry when infrastructure costs — CPUs, RAM, GPUs — are higher than historical norms.

4. Tech Industry and Energy: Nvidia’s Nuclear Energy Statements

A growing dimension of the semiconductor and AI infrastructure story is power demand. Advanced computing — especially AI training and inference — consumes vast amounts of electricity. Nvidia CEO Jensen Huang has publicly stated that future energy needs for AI infrastructure will require reliable, large-scale energy production such as nuclear power. Yahoo Finance+1

On platforms such as the Joe Rogan podcast, Huang has asserted that:

energy, not chips, may be the limiting factor for future AI growth and that small nuclear reactors near data centers could become a practical solution within the next decade because traditional grids may not scale fast enough. SightLine | U308+1

This echoes broader industry concerns that existing power infrastructure is strained and cannot reliably support the next waves of data-center-scale computation without significant upgrades.

Note: Huang’s comments do not imply Nvidia owns nuclear plants or that nuclear energy will immediately replace other sources — rather, he highlights the need for stable and scalable energy to support AI’s continued growth.

5. India’s Nuclear Policy Shift and Private Sector Entry

Contrary to outdated policies, the Indian government is now planning to open its nuclear energy sector to private players. This marks a significant policy shift from the historic, public-sector-dominated model. The Times of India+1

Key points:

- India’s **Atomic Energy Bill, 2025,**are proposes to allow private participation in nuclear power generation, supply, and infrastructure.

- The aim is to scale nuclear capacity from the current level significantly to meet rising energy demands, including those from industry and data centers. The Times of India

This is a strategic move to:

- attract long-term capital into energy infrastructure,

- complement renewable energy targets,

- and address the growing power requirements of computing infrastructure.

This is different from foreign nuclear plants being built by NPCIL (public sector) — but rather enables private firms to build and operate reactors.

6. Deeper Cause: Global Supply Chain Shifts & Geopolitics

Semiconductors are a global industry, and geopolitical strategies strongly influence resource flow, pricing, and investment decisions.

China’s push to dominate advanced industries — including semiconductor fabrication, AI, and nuclear technology — has been documented by global industry analysts as a long-term competitive strategy. itif.org

At the same time, export control regimes, policy shifts, and national security considerations have fragmented the once highly globalized supply chain, pushing some firms to localize supply and drive up costs.

7. What Happens Next?

Short-Term (1–2 years)

- Continued pricing pressure on high-end components

- Longer lead times

- Higher costs for enterprise IT budgets

- Continued focus on energy infrastructure investment

Mid-Term (3–5 years)

- Significant investments in nuclear and renewable energy to support intensive computing

- Private sector entry into previously state-controlled energy domains (e.g., India’s nuclear policy)

- Continued policy incentives for domestic semiconductor manufacturing (e.g., India’s Semicon Mission)

Long-Term (5–10 years)

- Expanded global megawatt-scale power sources — including nuclear — potentially co-located with data centers

- More robust, localized semiconductor ecosystems are reducing some supply volatility

- Mature AI and compute ecosystems balancing energy, performance, and sustainability

Conclusion

Electronic component price increases — from RAM to high-performance processors — are not isolated spikes, but the outcome of structural global shifts:

- semiconductor supply chain complexities,

- geopolitical restrictions,

- sharply rising compute and energy demand,

- and changing energy infrastructure needs.

Industry leaders like Nvidia’s Jensen Huang warn that energy, not just chips, will become a critical limiter of AI progress. This has pushed conversations about nuclear power and other base-load energy into mainstream strategic planning.

Meanwhile, policy changes like India’s move to open nuclear energy to private players represent a recognition that future energy and technology ecosystems must adapt to rising demands, both computational and economic.

Understanding these interconnected trends — from silicon to power production — is essential for readers, developers, businesses, and policymakers in 2025 and beyond.

References

- Overview of the semiconductor supply chain and complexity. ORF Online

- Nvidia’s CEO comments on nuclear power and AI energy demand. Yahoo Finance+1

- Global commentary on Nvidia CEO’s nuclear power perspective. SightLine | U308+1

- India’s plans to open the nuclear energy sector to private firms. The Times of India+1

- Context on nuclear policy and energy infrastructure

More in technology

Venture

Write for entrepreneurs, founders, and builders.

Share startup lessons, growth tactics, and founder stories with readers on the same journey.

One free account across In Plain English, Stackademic, Venture, and Cubed.

How it works- Startups & entrepreneurship

- Marketing & growth

- Productivity & leadership

- Founder stories & lessons learned

Sign in

Google or GitHub

Complete profile

Takes a few minutes

Get approved & publish

Start sharing

Why write for Venture?

Entrepreneurship is rarely a straight path. The lessons worth sharing are learned while building.

Frequently Asked Questions

Common questions about this topic

What are the primary root causes of sustained increases in electronics prices?

Sustained electronics price increases are driven by a combination of semiconductor supply chain complexity, surging demand for advanced chips (AI accelerators, edge and high-performance processors), slow capacity expansion for leading-edge fabs, geopolitical export controls, and rising energy costs and infrastructure constraints.

How does semiconductor supply chain complexity contribute to higher prices?

Semiconductor manufacturing depends on a highly specialized, interdependent global ecosystem—from raw materials and fabrication to EUV tools, packaging, and logistics—so disruptions in any link (for example in Taiwan or Japan) create scarcity that reverberates across the chain and raises prices.

Why is fabrication capacity for advanced nodes constrained and expensive to expand?

Building new fabs for leading-edge nodes (5nm, 3nm, and below) takes years and requires billions of dollars in capital, creating a structural mismatch when demand increases rapidly for AI, electric vehicles, and cloud services.

What role do geopolitical restrictions play in electronics price inflation?

Export controls and policy-driven restrictions on advanced lithography and chips reduce the global supply of high-end silicon, fragment the supply chain, and place upward pressure on prices by limiting the pool of available technology and capacity.

How do energy costs and infrastructure constraints affect semiconductor and data center economics?

Chip manufacturing and data-center-scale computing are energy-intensive; rising or unstable power costs increase operating expenses, and constrained or inadequate power infrastructure forces costs to be passed down the value chain or prompts investments in new energy capacity.

What consumer-facing symptoms indicate electronics price pressure is ongoing?

Visible symptoms include elevated retail prices for RAM modules despite seasonal expectations, sustained high prices for processors and GPUs (especially AI-oriented silicon), stretched lead times of weeks to months for mid- to high-end components, and increased activity in used electronics markets.

Which industries are most directly impacted by higher electronics prices and how?

Consumer electronics face reduced affordability for laptops, smartphones, and gaming PCs; enterprise IT and data centers encounter higher CapEx and delayed refresh cycles; automotive and IoT sectors see increased vehicle production and feature costs; and startups and R&D budgets face higher barriers to entry because infrastructure components are more expensive.

What has Nvidia CEO Jensen Huang said about energy and AI infrastructure?

Jensen Huang has stated publicly that energy, rather than chips, may become the limiting factor for future AI growth and suggested that small nuclear reactors near data centers could be a practical solution within the next decade because traditional grids may not scale fast enough.

Do Jensen Huang’s statements imply Nvidia owns or will immediately build nuclear plants?

No, the statements emphasize the need for stable, scalable energy to support AI growth and do not imply Nvidia owns nuclear plants or that nuclear energy will immediately replace other energy sources.

What change is occurring in India’s nuclear energy policy?

India is planning to open its nuclear energy sector to private players through measures such as the Atomic Energy Bill, 2025, enabling private participation in nuclear power generation, supply, and infrastructure to attract long-term capital and scale capacity to meet rising energy demands.

How is the private-sector entry into India’s nuclear sector intended to interact with computing and energy needs?

Private-sector entry is intended to attract long-term capital into energy infrastructure, complement renewable targets, and help address growing power requirements from industry and data centers that support intensive computing workloads.

What short-, mid-, and long-term expectations are outlined for electronics pricing and energy investment?

Short-term (1–2 years): continued pricing pressure on high-end components, longer lead times, higher enterprise IT costs, and focus on energy infrastructure investment. Mid-term (3–5 years): significant investments in nuclear and renewables for intensive computing, private-sector entry into energy domains, and continued incentives for domestic semiconductor manufacturing. Long-term (5–10 years): expanded megawatt-scale power sources potentially co-located with data centers, more localized semiconductor ecosystems reducing some supply volatility, and mature AI/compute ecosystems balancing energy, performance, and sustainability.

Comments

Loading comments…